All

News

Trends

Offers

Debt Consolidation Loans in Germany: How They Work

Debt consolidation loans help you combine many debts into one simple loan. Instead of paying several credit cards, overdrafts, or small loans, you pay only one monthly instalment. In Germany, this type of loan is usually offered as an unsecured personal loan. Many people choose debt consolidation because it feels easier to manage and can reduce stress. In this article, you will learn how debt consolidation loans work in Germany, how banks calculate costs, and what role APR (Annual Percentage Rate) plays. We explain why combining debts can lower your monthly payment but sometimes increases the total amount you pay. You will also learn how German banks check your application and what happens after approval. The goal is to help you understand how debt consolidation works so you can decide if it fits your situation. By the end, you will know how to use a consolidation loan responsibly and avoid common mistakes.

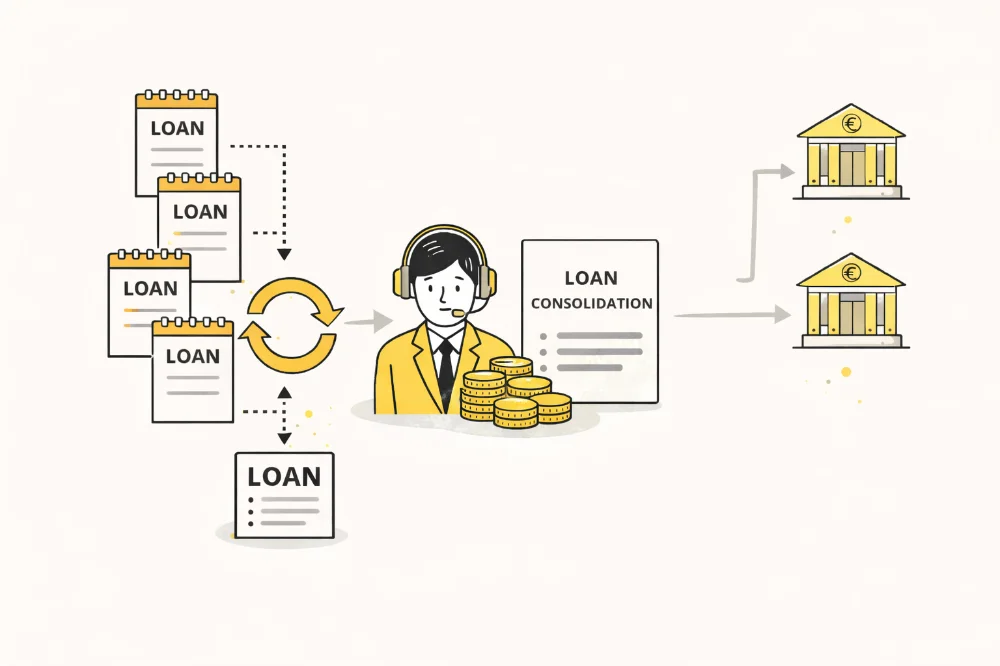

What a debt consolidation loan is in Germany

A debt consolidation loan is a personal loan used to repay other debts. In Germany, it is usually an unsecured loan. This means you do not need to provide a house or car as collateral. The bank gives you a fixed amount of money. You use this money to pay off your existing debts. Many people in Germany have several types of debt. These can include credit cards, overdrafts on a current account, instalment loans, or store financing. Each debt has its own interest rate and payment date. This can be confusing and stressful. A consolidation loan turns all these payments into one loan with one due date. For example, you might owe €2,000 on a credit card, €1,500 on an overdraft, and €3,500 on a small consumer loan. Together, this is €7,000. Instead of paying three different lenders, you take one consolidation loan for €7,000. You then pay one monthly instalment to one bank.

In Germany, banks usually offer consolidation loans with fixed interest rates and fixed monthly payments. This makes planning easier. You know exactly how much you pay every month and when the loan ends. Most consolidation loans have terms between 12 and 84 months. The bank does not always pay your old debts automatically. Sometimes you receive the money in your account and must repay the old debts yourself. Some banks offer a service where they pay the old lenders directly. This can help you avoid using the money for other purposes.

A consolidation loan can lower your monthly payment. This happens when the new loan has a lower APR than your old debts. Credit cards and overdrafts in Germany often have very high interest rates. A personal loan usually has a lower rate. This difference can save money each month. However, consolidation does not remove your debt. It only changes how you repay it. If you extend the loan term, you might pay more interest in total. A lower monthly payment can feel good, but the total cost matters too. In Germany, banks must clearly show the APR and total repayment amount. This helps you compare offers. You should always check the total amount you will repay, not only the monthly instalment.

Debt consolidation works best when you stop creating new debt. If you continue using your credit card or overdraft, your debt can grow again. The loan helps only if you change how you manage money. A consolidation loan is not a miracle solution. It is a tool. Used correctly, it can make your finances simpler and more transparent. Used incorrectly, it can delay problems instead of solving them.

How banks in Germany calculate costs and APR

In Germany, the most important number for a loan is the APR. APR means Annual Percentage Rate. It shows the yearly cost of the loan, including interest and most fees. Banks must display this rate clearly. The APR depends on several factors. One factor is your credit profile. Banks check your income, expenses, and credit history. If the bank sees low risk, you get a lower APR. If the risk is higher, the APR increases. Another factor is the loan amount and the loan term. Shorter loans usually have higher monthly payments but lower total interest. Longer loans have lower monthly payments but higher total interest. For example, a consolidation loan of €10,000 with an APR of 6% over 3 years might cost about €1,000 in interest. The same loan over 6 years might cost about €2,000 in interest. The monthly payment is lower, but the total cost is higher.

Banks also look at how stable your income is. A permanent job contract often helps. Self-employed people may need to show more documents. Pensions and regular benefits can also count as income. Some lenders charge additional fees. These can include processing fees or optional insurance. In Germany, most modern lenders include these costs in the APR. This makes comparison easier. When you apply, the bank calculates a monthly instalment. This instalment includes interest and repayment of the principal. At the beginning, a larger part of the payment goes to interest. Over time, more goes to repaying the debt. You should always look at the total repayment amount. This is the amount you will pay back including interest. Two loans can have the same monthly payment but different total costs because of different loan lengths.

German law requires clear information. Before you sign, you receive a standard information sheet. It shows the APR, monthly payment, total amount, and contract duration. This document helps you compare offers from different banks. APR can be fixed or variable. Most consolidation loans in Germany use a fixed APR. This means the rate does not change during the loan term. This gives security and predictable payments.A lower APR does not always mean a better loan. If the loan term is much longer, you may still pay more overall. Always combine APR and term when comparing offers.

Understanding how banks calculate costs helps you avoid surprises. It also helps you choose a loan that matches your budget and long-term plans.

The application and approval process in Germany

Applying for a debt consolidation loan in Germany is usually simple. Most banks and online lenders offer digital applications. You enter the loan amount, loan purpose, and personal data. You must provide information about your income and expenses. Banks want to see that you can afford the monthly payment. You may need to upload payslips or bank statements.

In Germany, the bank also checks your credit history in SCHUFA. The bank looks at past loans, payment behaviour, and existing debts. This check helps the bank decide the APR and whether to approve the loan. After the check, you receive an offer. This offer shows the loan amount, APR, monthly payment, and total repayment. You should read it carefully. If you agree, you sign the contract digitally or on paper. After signing, the bank pays out the money. This can happen within a few days. Some lenders send the money directly to your old creditors. Others transfer it to your account. If the money comes to your account, you should repay your old debts immediately. This prevents double interest. It also helps your credit profile because old accounts are closed.

Many loans in Germany allow early repayment. This means you can pay extra or finish the loan early. Some banks charge a small fee for this. You should check this in the contract. The approval process is faster than in the past. Fintech lenders can approve loans in minutes. Traditional banks may take longer but often offer personal advice. The most important part of the process is honesty. If you hide debts or income problems, the bank may reject the application or give worse conditions.

A consolidation loan is a new financial commitment. You should be sure the monthly payment fits your budget even if your situation changes slightly. When used correctly, the application process is a chance to reset your finances. You replace many chaotic payments with one structured plan.

Benefits, risks, and conclusion

Debt consolidation loans have clear benefits. They simplify your finances. You pay one instalment instead of many. This reduces the risk of missing a payment. It also makes budgeting easier. They can also lower your monthly burden. If your old debts had high interest rates, a consolidation loan with a lower APR can save money each month. This creates financial breathing room.

There are also risks. A longer loan term means more interest over time. A lower monthly payment can be tempting, but it may hide higher total costs. Another risk is behaviour. If you keep using credit cards or overdrafts after consolidation, your debt can increase again. The loan works only if you change spending habits. You should also be careful with insurance products. Payment protection insurance increases the total cost. It is not always necessary. Before choosing a loan, compare offers from different banks. Look at APR, total repayment, and flexibility. Make sure you understand all conditions. Debt consolidation is not for every situation. If debts are very high or income is unstable, other solutions may be needed. In such cases, professional advice can help.

In conclusion, debt consolidation loans in Germany help combine many debts into one structured loan. They can reduce stress and improve clarity. They can also lower monthly payments if the APR is better than before. However, they do not erase debt. They only change how it is repaid. Used wisely, a consolidation loan can be a strong tool for regaining control over your finances and planning a more stable future.

Author: Moini

28/03/2026, 3 min read