All

News

Trends

Offers

How Banks in Germany Assess Your Creditworthiness

When you apply for a loan or a credit card in Germany, banks do not guess whether to approve you. They calculate your creditworthiness using clear rules and data. Creditworthiness means how safe you look as a borrower. It shows the bank how likely you are to repay your money on time. Many people think this decision is random. It is not. Banks use your financial history, your income, and your current obligations to build a risk profile. They also use data from the credit bureau SCHUFA. A good profile means better chances for approval and lower interest rates. A weak profile means higher costs or rejection. This article explains in simple language how banks in Germany calculate your creditworthiness. You will learn what information they use, how they evaluate your risk, and how your daily financial habits affect the result. Understanding this process helps you prepare before you apply for a loan. It can save you money and prevent unpleasant surprises. After reading, you will know what banks look at and how you can improve your financial image.

What Creditworthiness Means for German Banks

Creditworthiness is how banks measure the risk of lending money. In simple terms, it answers one question: will you repay your loan as agreed? In Germany, this evaluation is based on data, not assumptions. Banks examine your past financial behavior to predict future reliability. If you consistently paid bills and loans on time, you appear trustworthy. Conversely, missed payments or defaults make you look risky, potentially affecting your ability to borrow.

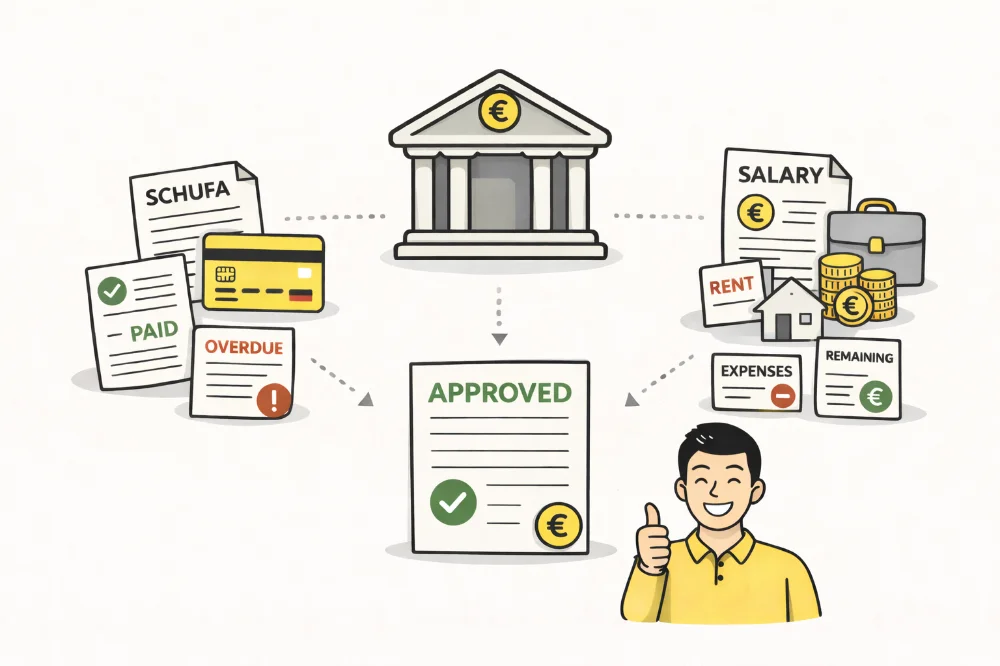

Banks assess creditworthiness using two main components. The first is your payment history, which shows how you managed debts in the past. The second is your current financial situation, which indicates whether you can afford new monthly payments today. Both aspects are equally important. Payment history comes primarily from SCHUFA, Germany’s main credit bureau. SCHUFA tracks loans, credit cards, and any unpaid bills. It does not know your income, only whether you paid on time. Banks use this information to identify patterns of financial reliability or past problems.

Your current financial situation is evaluated directly by the bank. They review your income, type of employment, length of employment, and fixed monthly costs like rent, existing loans, or child support. The remaining amount, called “free income,” shows how much money is available to repay a new loan. Even with a strong SCHUFA score, low free income can reduce your creditworthiness. Likewise, a high salary cannot fully compensate for a poor SCHUFA record. Banks combine both perspectives to make a final decision, balancing historical reliability with present affordability.

Creditworthiness is not permanent—it changes with your circumstances. Getting a higher-paying job, reducing debts, or maintaining timely payments can improve your score, while missed payments or taking on multiple loans can lower it. In Germany, this system is strict because banks must follow responsible lending rules. They are legally required to assess risk and avoid giving loans to those unable to repay them. This protects both the bank and the borrower from serious financial problems.

Which Data Banks Use to Calculate Your Creditworthiness

Banks in Germany rely on multiple types of data to calculate your creditworthiness. The most important external source is SCHUFA, the country’s main credit bureau. SCHUFA provides both a score and detailed information about your contracts, including loans, credit cards, and any past payment problems. Banks pay particular attention to negative signals, such as unpaid bills, collection cases, or insolvency records. They also consider how many contracts you have open—many active credit lines can indicate risk, while long-standing, stable contracts generally signal reliability and financial responsibility.

Internally, banks assess the information you provide in your loan application. This includes your monthly income, employment type, and job stability. Permanent employment is considered more reliable than temporary work, while self-employed income is accepted but usually examined more carefully. Banks also review your fixed expenses, including rent, existing loans, leasing contracts, and family obligations. After subtracting these costs, they calculate your disposable income—the amount you have available for new payments. Other factors, like age and household size, are also taken into account. Younger borrowers may have less credit history, and larger households face higher living costs, both of which influence the evaluation.

Some banks additionally examine your account behavior. Frequent overdraft usage, rejected payments, or negative balances can reduce your internal rating, whereas stable account management supports a stronger evaluation. All this data is combined into a scoring model. Each factor carries a specific weight, with payment history usually having the greatest impact, followed by income stability, current debts, and living costs. The scoring system produces a risk category that summarizes your overall creditworthiness.

This risk category determines three critical outcomes: whether your loan is approved, the maximum amount you can borrow, and the interest rate you receive. A strong category signals low risk to the bank, leading to better conditions and lower interest rates. Conversely, a weak category can result in higher rates or outright rejection. In many banks, this process is automated, with computers calculating creditworthiness in seconds. Despite the automation, the principle remains straightforward: banks want assurance that you can and will repay your loan.

How Banks Turn Data into a Final Decision

After collecting all relevant data, the bank combines it into a single result known as your internal bank rating. While this rating is separate from your SCHUFA score, the two are closely connected. The internal rating is what the bank actually uses to make lending decisions. First, the bank checks your SCHUFA profile. Serious negative entries, such as unpaid debts or insolvency, often result in automatic rejection. If your SCHUFA record is acceptable, the bank proceeds to analyze your income in detail.

Next, the bank calculates your affordability. It subtracts your fixed costs—including rent, existing loans, and other financial obligations—from your income to determine how much money is available for a new loan payment. If your disposable income is insufficient to cover the expected loan installments, approval is unlikely. The bank also evaluates your overall stability. Long-term employment, stable residence, and consistent bank account behavior all improve this assessment, while frequent job or address changes can lower your rating.

Once all factors are considered, the system assigns you a risk class. Each risk class corresponds to a maximum loan amount and a minimum interest rate. This explains why two people applying for the same loan can receive very different offers. A higher-risk class may mean a smaller loan or higher interest, while a strong profile can lead to larger credit limits and more favorable rates. This system protects both the bank and the customer, ensuring that loans are manageable and that lending is responsible, as required by German financial regulations.

It is important to understand that banks do not judge you personally—they judge numbers and patterns. Your lifestyle, personality, or personal choices outside finance are irrelevant. What matters is your financial behavior. This also means that you can influence your internal rating. Paying bills on time, reducing debt, and maintaining stable contracts all improve your creditworthiness. In essence, creditworthiness is not determined by luck; it is the result of consistent, responsible financial decisions made every day.

How You Can Improve Your Creditworthiness in Germany

The best way to improve your creditworthiness is straightforward: pay all your bills on time. Late payments are the most negative signal for banks, and even small delays can damage your profile. Consistently meeting deadlines shows reliability and builds trust with lenders, which can lead to better loan conditions in the future.

Keeping your debts low is equally important. Avoid maxing out credit cards, as high utilization signals risk, while lower balances indicate stability. Limit the number of loan applications you submit in a short period. Each request is recorded, and multiple applications in quick succession may suggest financial stress. Space out applications and only apply when necessary to protect your credit profile.

Regularly monitoring your SCHUFA report is another key step. Errors or outdated information can reduce your score and your internal bank rating. Correcting inaccuracies improves your chances of approval. Stability in your employment and residence also contributes positively. Long-term jobs and consistent living arrangements signal reliability, while frequent changes can make you appear riskier to lenders.

Finally, understand that building strong creditworthiness is a gradual process. Use credit responsibly, repay loans as agreed, and prioritize paying off smaller debts first. Reducing monthly obligations over time strengthens your profile. German banks use structured systems that reward consistency and penalize financial disorder. By understanding these factors and managing them carefully, you can improve your chances of approval and secure lower borrowing costs.

Author: Moini

11/04/2026, 3 min read