All

News

Trends

Offers

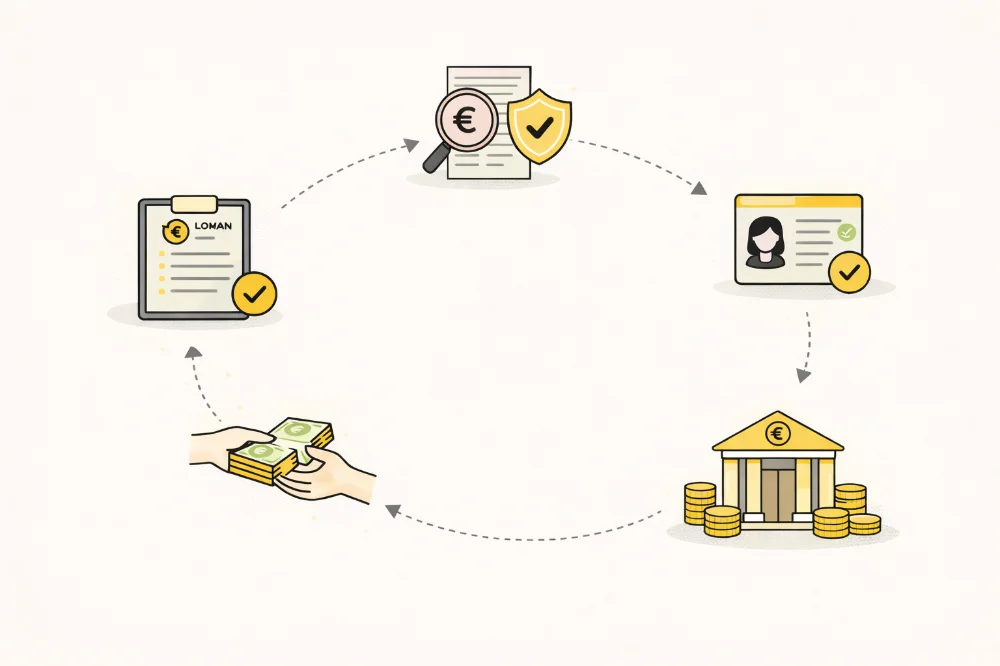

How Personal Loans Work From Start to Finish

Personal loans can be a helpful tool for funding big expenses, consolidating debt, or handling emergencies. But if you’ve never taken one, the process can feel confusing. In this article, we will explain exactly how personal loans work from start to finish. You’ll learn how to apply, how lenders evaluate your request, and what determines your interest rate and APR. We’ll also explain how the loan is disbursed, how repayments work, and what to do if you want to pay it off early. Along the way, we’ll cover common fees, risks, and mistakes people make, so you can avoid surprises. By reading this article, you’ll understand the entire journey of a personal loan in clear, simple language. You’ll know what to expect before you apply and how to manage your loan responsibly. This guide is written in plain language, like advice from German retail banks, online lenders, and fintechs, for anyone in Germany who wants to understand unsecured personal loans without financial confusion.

Applying for a Personal Loan

The first step is the application. Personal loans are usually unsecured, meaning you don’t have to provide collateral. To apply, you fill out an application form online or at a bank branch. You provide information about your income, employment, expenses, and sometimes your existing debts.

Lenders use this information to assess whether you can repay the loan. They may also check your credit score. A higher credit score usually increases your chances of approval and may help you get a lower APR. Some lenders can give a decision within minutes online, while others may take a few days.

When applying, you should compare offers from different lenders. Pay attention to the loan amount, term, and APR. Even a small difference in APR can affect how much you pay in interest over time. You can also check if there are any origination fees or early repayment penalties.

It’s important to borrow only what you need. Many people apply for the maximum allowed, but that increases monthly payments and interest. A personal loan should meet your needs, not create financial stress. Before submitting your application, gather all necessary documents. This can include payslips, bank statements, and ID. Being organized speeds up approval and reduces mistakes. Understanding the application process ensures you are prepared and increases the likelihood of getting a loan that suits your financial situation.

How Lenders Evaluate You and Set Your APR

After applying, the lender evaluates your creditworthiness. They look at your income, job stability, existing debts, and sometimes your banking history. The goal is to estimate how likely you are to repay the loan on time.

Your APR, or annual percentage rate, depends on this evaluation. A higher credit score and steady income usually mean a lower APR. Lenders also consider the loan term and amount when setting the interest rate. Even small differences in APR can change the total cost significantly over the life of the loan.

Some lenders charge fees in addition to interest. These can include origination fees, late payment fees, or prepayment penalties. Make sure you understand all fees before accepting a loan.

Riskier applicants may still get approved, but often with a higher APR. That is why it’s important to be honest about your financial situation and only borrow what you can repay. Being aware of how lenders assess you helps you prepare for approval. Checking your credit report in advance, paying off small debts, and ensuring stable income can improve your chances of a favorable APR.

Disbursement and Managing Your Loan

Once approved, the lender disburses the loan. The funds are usually transferred to your bank account within a few days. You can use the money for your intended purpose, such as home improvements, medical bills, or debt consolidation.

Repayment starts according to the agreed schedule. Most personal loans are repaid in fixed monthly installments that cover both interest and principal. The APR tells you the total cost of borrowing over a year. Paying on time is crucial to avoid late fees and negative marks on your credit report.

Many lenders allow early repayment. Paying off your loan early can save interest, but check for prepayment fees. Some loans include penalties if you repay too quickly, so always read the terms. Tracking your loan helps you stay on top of payments. Using apps, automatic transfers, or calendar reminders can make it easy to avoid late payments. Budgeting for the monthly installment ensures you don’t overextend yourself.

If you face financial difficulties, contact your lender immediately. Many lenders offer temporary solutions, such as payment deferrals or adjusted schedules. Ignoring the loan can worsen your situation and increase interest costs. Managing your personal loan responsibly allows it to be a tool for financial flexibility rather than stress. Understanding the process from disbursement to repayment ensures you know exactly what to expect.

Tips, Mistakes, and Conclusion

Common mistakes include borrowing more than you need, missing payments, and ignoring fees. These errors increase costs and make repayment stressful.

To avoid mistakes, plan your loan carefully. Only borrow what you can repay comfortably, understand your APR, and factor in all fees. Compare lenders to get the best terms. Keeping a repayment schedule and using automatic payments helps you avoid missed payments. If possible, pay more than the minimum installment to reduce total interest.

Finally, think ahead. A personal loan is a short-term solution, not a long-term crutch. Use it wisely to fund necessary expenses or consolidate higher-interest debt.

In conclusion, personal loans work from start to finish through a clear process: application, evaluation, approval, disbursement, and repayment. By understanding each step, APR, and fees, you can manage your loan responsibly. Planning, comparing offers, and tracking payments ensures the loan helps you rather than creating financial stress.

Author: Moini

17/02/2026, 3 min read