All

News

Trends

Offers

Why Your Credit Score Changes Every Day and How AI Credit Insights Help You Track It in Real Time

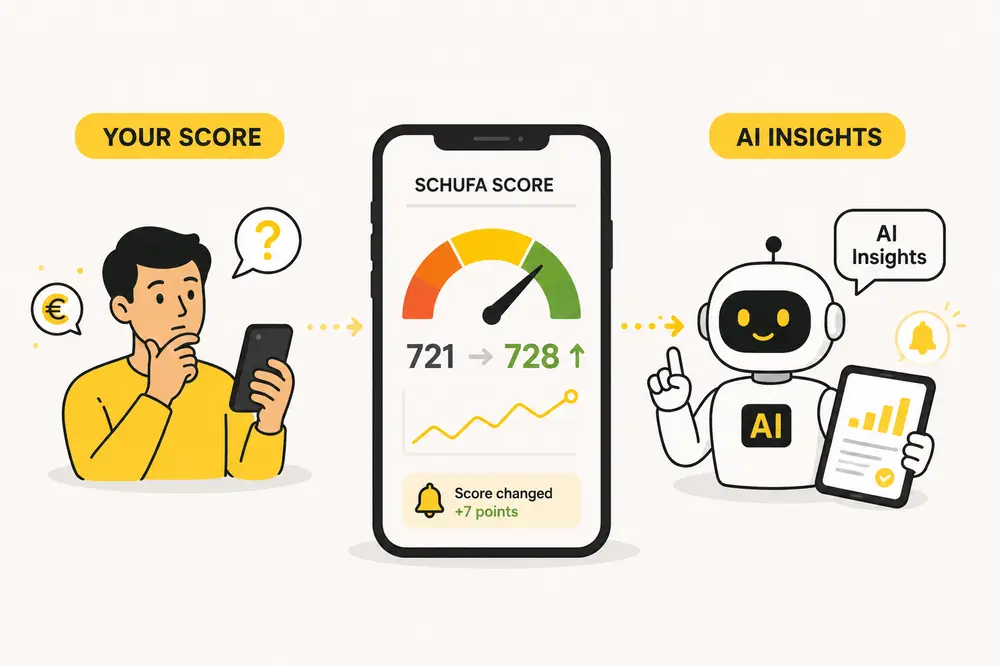

Most people think their credit score changes only when they miss a payment, but that is not true. In Germany, your SCHUFA profile can shift because of new data, old data disappearing, credit checks, open accounts, and lender behavior. What nobody tells you is that real-time AI credit insights can help you notice small changes before they become expensive.

Why your credit score can change even when you do nothing

Your credit score is not a fixed grade. It is more like a financial snapshot that gets refreshed when new information reaches a credit bureau, a lender checks your file, a bank account ages, a loan balance changes, or an old entry stops being relevant. In Germany, many people connect this mainly with SCHUFA, because SCHUFA data is often used when applying for loans, credit cards, mobile contracts, and sometimes rental documents. SCHUFA says its classic score values can run from 0 to 100%, where a higher score indicates stronger creditworthiness and lower risk of non-payment. It also states that banks may consider other factors, such as disposable household income, when making lending decisions.

The confusing part is that you may not see the same picture a lender sees. For example, you might check a credit report because a landlord asks for it, while a bank may look at a different credit product score or combine SCHUFA data with its own internal affordability model. That is why reading a single number without context can be misleading. If you are new to this topic, understanding how banks decide whether to approve a loan helps you understand what to expect beyond the score itself, because lenders usually care about income, monthly obligations, employment type, and repayment behavior too. This internal topic already appears in the Moinify English article database, alongside SCHUFA, personal loans, credit cards, budgeting, and cost guides, which shows that the new angle here should focus on daily score movement and AI tracking rather than repeating general SCHUFA basics.

In practice, your score can move for small reasons. A paid-off loan may reduce risk, but closing an old account can also remove a long positive history. A new credit card can improve available credit, but several applications close together may look risky. A late payment can hurt quickly, while a corrected mistake can help once the update is processed. Many people search for SCHUFA report or improve SCHUFA score only after a rejection, but the better approach is to monitor changes before applying.

What is interesting is that not every daily movement matters. A small score change may simply reflect data refreshes, while a sudden drop deserves attention. If you notice a new inquiry, an account you do not recognize, or an old unpaid item that should already be resolved, it is worth checking the source. One small data issue can become very real: on a €10,000 loan, moving from an approximate 7% APR to 11% APR over 48 months can add roughly €850 in extra interest, depending on the lender and repayment plan.

What AI credit insights can see faster than you can

AI does not magically improve your credit score. A useful AI credit insights tool does something more practical: it watches patterns, organizes information, and explains what changed in plain language. Instead of forcing you to open several banking apps, read a SCHUFA document, compare loan balances, and guess what matters, AI can turn scattered data into a short explanation such as: your credit card utilization rose, a loan inquiry appeared, one account balance dropped, or your repayment pattern improved.

This matters because many people do not fail financially because of one big mistake. They lose control through small, invisible changes. Maybe your overdraft is used for ten days every month. Maybe your credit card balance keeps sitting near the limit. Maybe you opened two “buy now, pay later” plans and forgot that they still affect your monthly budget. A real-time system can notice these patterns before you apply for a loan, before you request a credit report, or before you start comparing financial products in tools like wiso mein geld. The point is not to scare you, but to make the invisible visible.

A simple comparison helps:

AreaManual trackingAI credit insightsSpeedYou check when you rememberAlerts can appear soon after a changeExplanationYou interpret documents yourselfChanges are summarized in simple languageBudget linkOften separate from credit scoreSpending, income, and debt patterns can be connectedRisk warningUsually lateCan flag behavior before it becomes a problem

AI credit tools are becoming more important because lenders themselves are also using more data-driven systems. Under the EU AI Act framework, AI systems used to evaluate creditworthiness or establish credit scores are treated as high-risk when they affect access to essential private services, although implementation timing and obligations continue to evolve. For everyday users, the practical takeaway is simple: AI can help with credit awareness, but any tool that uses sensitive financial data should be transparent, explainable, and careful with consent.

There are two things beginners should look for:

The tool should explain why a change happened, not only show that a number moved.

The tool should separate harmless updates from urgent risks, such as missed payments, unknown inquiries, or rising debt pressure.

The best use case is not “AI tells me I am good or bad.” It is more like a calm financial assistant that says: this changed, here is why it may matter, here is what you can do next. If you also use a credit card limit assessment tool to get a clearer estimate of monthly repayment pressure, the picture becomes much easier to understand because your score behavior and your real cash flow are finally connected. The Moinify calculator list includes credit card, loan, salary, savings, interest, and car loan tools, so this article can naturally support the tools cluster without inventing links.

The real cost of not tracking your credit score

Credit score tracking sounds boring until it affects a real price. In Germany, a stronger risk profile can make it easier to access a normal installment loan, while a weaker or unclear profile can mean higher APR, more documents, a smaller approved amount, or a rejection. Exact loan pricing depends on the lender, term, income, employment type, credit history, and current market conditions. Bundesbank statistics track German bank consumer loan interest rates as annual percentage rates of charge, which is the kind of cost measure borrowers should compare when reviewing offers.

Here is an approximate cost breakdown. Imagine a beginner borrower in Germany wants €12,000 over 48 months. With a clean profile, stable income, and no recent warning signs, an approximate APR of 6.5% could mean a monthly payment near €284 and a total repayment near €13,630. With a weaker profile, unclear debt pressure, or a recent negative signal, an approximate APR of 10.5% could mean a monthly payment near €307 and a total repayment near €14,740. The difference is about €1,110 over four years. That is not abstract. That could be a year of public transport tickets in many cities, several months of electricity bills, or the emergency buffer someone never manages to build.

This is where human behavior matters. Many people check their score after the expensive moment, not before it. They apply, get rejected, panic, search SCHUFA, search SCHUFA report, then try to understand what happened. A better sequence is calmer: check your current credit picture, correct obvious errors, reduce avoidable debt pressure, compare costs, then apply. If the goal is to borrow, using a calculation tool gives you a better idea of monthly payments before a lender makes the decision for you. That calculator appears in the approved Moinify English calculator list, so it fits the middle of the article as a tool link rather than a random call to action.

The cost is not only loan interest. A poor or unclear credit profile can create friction in everyday life. A mobile contract may require prepayment. A credit card limit may stay low. A landlord may ask for extra reassurance. A bank may approve a smaller overdraft or none at all. And what is interesting is that people with good income can still run into problems if their data story looks unstable. A freelancer earning €4,500 a month but showing irregular cash flow, repeated overdraft use, and several recent applications may look riskier than an employee earning €2,700 with predictable salary payments and clean repayment behavior.

There is also an opportunity cost. If you miss a wrong entry or a sudden score drop for three months, you may delay a loan application, accept a more expensive offer, or avoid applying altogether. This is why AI credit insights are useful for beginners: they reduce guesswork. They do not promise approval, and they should not. But they can help you notice when your behavior is moving in the right direction. If you are also learning how to save, even a simple instant-access savings account can support your credit story indirectly, because a growing cash buffer reduces overdraft use and makes your monthly finances less fragile.

How to use AI tracking without becoming obsessed with the score

The danger of real-time tracking is that people can start treating every small movement like an emergency. That is not healthy, and it is not necessary. A credit score is important, but it is not your full financial identity. The useful habit is to review changes weekly, check alerts when something unusual happens, and focus on actions that improve your real financial position: pay on time, keep balances manageable, avoid unnecessary applications, and build a small savings buffer.

A practical routine is simple. First, check your credit data before major applications, especially before a loan, credit card, rental process, or car financing. Second, use AI explanations to understand the reason behind a change. Third, compare the score signal with your real budget. A score can look fine while your monthly cash flow is under pressure, and the opposite can also happen. If credit card debt is part of the picture, reading about minimum payment costs provides a clearer picture of why small monthly payments can quietly become expensive over time.

There is one more beginner mistake: trying to “game” the system. Searching improve SCHUFA score is common, but the honest answer is usually less exciting than people hope. Pay bills on time. Keep old healthy accounts where they still make sense. Avoid many credit applications in a short period. Do not use your overdraft as a second salary. Check whether entries are correct. SCHUFA has also introduced newer score information with point ranges in its transparency material, including classes such as excellent, good, acceptable, and sufficient, which shows how much the market is moving toward clearer explanations rather than mystery numbers.

Real-time AI credit insights work best when they help you make fewer emotional decisions. The goal is not to watch the number every morning; the goal is to understand what financial behavior the number is reflecting. In conclusion, your credit score may change often, but your strategy should stay calm and consistent. When you combine SCHUFA awareness, simple budgeting, and real-time AI explanations, you give yourself a better chance of spotting problems early and saving real money before they become expensive.

FAQ: Common Questions About Changes in Credit Score

Why does my credit score change every day?

Your credit score can change when new credit data appears, old data is updated, balances move, inquiries are added, or negative information is corrected or removed.

Does checking my own SCHUFA score lower it?

Checking your own SCHUFA information should not lower your score. Problems usually come from lender application checks or risky financial behavior, not from viewing your own data.

Can AI improve my credit score?

AI cannot directly improve your credit score, but it can show which habits may be hurting it. That makes it easier to act early.

What is the difference between credit report and SCHUFA report?

A credit report is usually a creditworthiness document used to prove reliability, while a SCHUFA report often refers more broadly to SCHUFA information or a data report.

How can I improve my SCHUFA score in Germany?

Pay bills on time, avoid repeated credit applications, keep debt manageable, correct wrong entries, and build stable account behavior over time.

Author: Moini

14/05/2026, 3 min read